Over the many years I’ve been in business, a regular reading and studying of the basic economic indicators has helped to me see the rhythm of how our economy works. As a credit professional, allow me to share with you my general understanding of the top three indices and how they play into our credit decisions.

First, my choice for the top three economic indices which I generally look at to evaluate how our economy is doing are:

- gross domestic product (GDP)

- unemployment rate

- inflation rate

Personally, I think GDP is the most important since the other indicators tend to rise and fall depending on what’s happening with GDP.

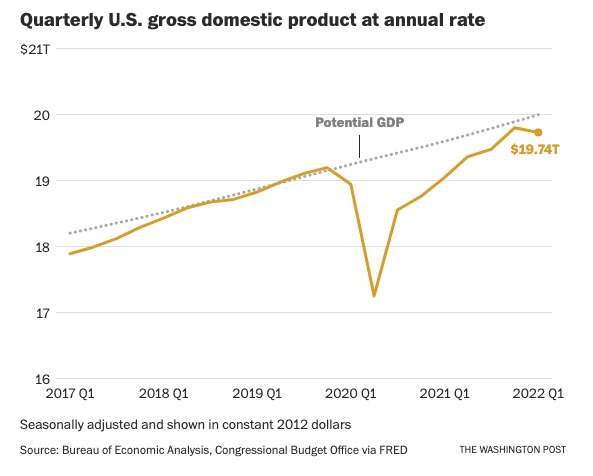

As a refresher, GDP is the value of all goods and services produced in the economy and the broadest measure of economic activity. It’s measured by adding up the various categories of spending in the economy. These broadly include: consumer spending, investment spending, government spending, and net exports. Please note the GDP trend from 2017 Q1 though 2022 Q1.

Let me mention a quick thought on the meaning of net exports.

The net exports part of GDP for the United States has been negative for the past several decades and that’s because the U.S. imports more goods and services than it exports. However, if we separate the value of goods from services, we import more goods than we export, but we export more services than we import.

One more note on net exports — since the importation of foreign goods is larger than the export of our services, the offset between the two results in a net negative trade balance, or what is termed a trade deficit.

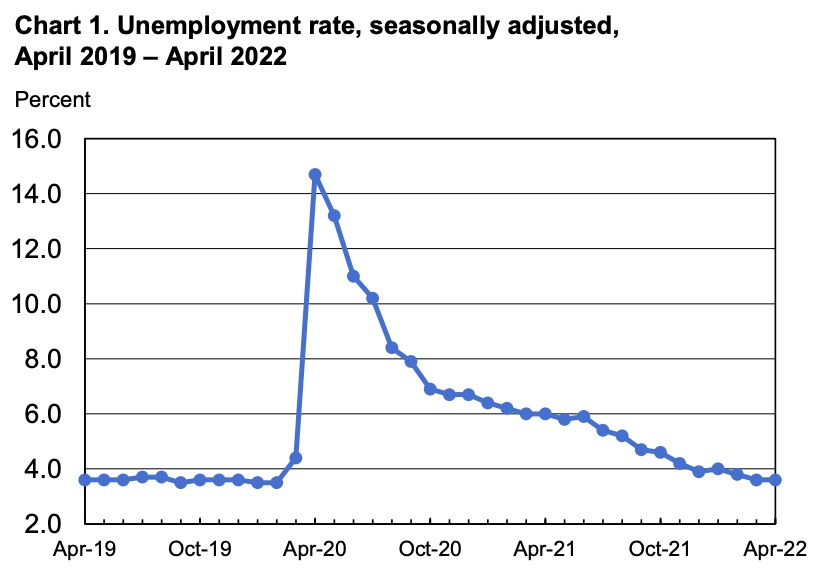

The next important economic indicator is the unemployment rate. This measures the number of people who are unemployed but are still actively seeking employment, as a percentage of the total labor force. The total labor force includes all those who are working plus all those who are unemployed but are still actively seeking work.

One interesting note that I discovered is that the unemployment rate is measured through a household survey and not by the number of people collecting unemployment insurance. So even if someone whose unemployment benefits run out, they will still be included in the number of unemployed if they are actively searching for a job. Please see the unemployment rate from April 2019 – April 2022.

Typically, when GDP declines, the unemployment rate rises. The reason is that, if we are producing fewer goods and services, we need fewer workers. Conversely, when GDP increases, we need more workers, so the unemployment rate drops.

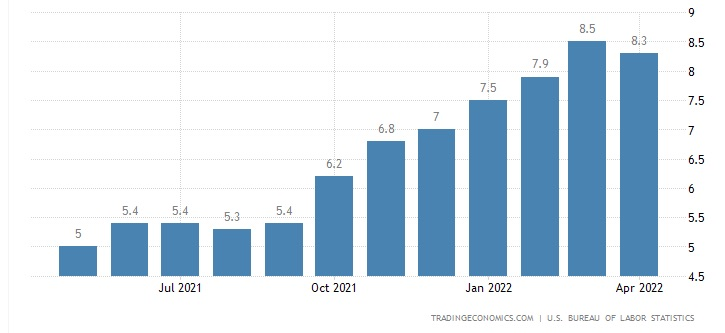

The third measure I believe is the inflation rate, which as you know full well, we are experiencing head on. There are several measures of inflation, but the most widely used is the Consumer Price Index. Please see the inflation rate from April 2021 to April 2022.

From my understanding, there are two main causes for inflation. The first has primarily to do with the price of oil. The global economy runs on oil and as it rises, it causes other prices for a multitude of direct and indirect products to rise. This cause of inflation is technically termed, “cost-push inflation.”

Cost-push inflation can occur at any time and is most often related to world events. Storms, natural disasters, and international crises, such as the current turmoil in the Ukraine, can drive up oil prices and therefore the prices of other goods and services.

When cost-push inflation occurs at the same time as a decline in GDP and a rise in unemployment, it tends to wreak havoc in the economy because it further reduces the amount of goods and services demanded, which then further drives down GDP and increases unemployment.

The other cause for inflation occurs when production in the economy can’t keep up with spending. The term for this is “demand-pull inflation.” This is more commonly known as “too many dollars chasing too few goods,” which causes prices to go up. Think in terms of the current housing situation in which supply cannot keep up with demand, and in several areas of the US, home prices continue to skyrocket.

Demand-pull inflation occurs when GDP is strong, and unemployment is low. The reason is that as more people are working and feeling secure in their jobs, they also feel encouraged to purchase more. So there tends to be a tradeoff between unemployment and inflation. When unemployment is low, in which people are actively buying products and services outpacing supply, inflation is high (or increases). Conversely, when unemployment is high and people are out of work, spending decreases, demand decreases, and inflation (prices of goods and services) comes down.

So where does this leave the credit professional? Our current and prospective customers, as well as and our own businesses, are affected either directly or indirectly by the economy’s ebbs, flows, peaks and valleys. Understanding the basics of how the economy works is how we can begin to anticipate how our customers and clients may be challenged, which in turn affects their ability to meet their financial obligations. To get a clearer understanding of your customers, you may want to do a little analysis and group your customers by:

- Industry – try to ascertain to what extent in the supply chain they rely on oil in their manufacturing or distribution process.

- Employee number – try to project their employee increases and decreases during inflationary and non-inflationary times.

- Location – try to anticipate if there is a propensity for a natural disaster or political upheaval to adversely affect them.

The more you can understand the macroeconomic factors that could impact your customers, the better you will be able to anticipate what kinds of credit changes may be necessary to implement.

Your questions and comments are most welcome (nseiverd@cmiweb.com).

All Rights Reserved