As originally published in the Credit Research Foundation 2Q 2019 CRF News.

Have you ever thought about from where the concept of benchmarking originated? Like most people, I never really gave it much thought. But interestingly, way back in the days before mass production and high tech equipment, adjustments to correct the performance of a firearm were carried out on a workbench. Thus the word “benchmarking” referred to the fine modifications necessary for a firearm to perform with accuracy. Over time, the term “benchmarking” evolved into the idea of businesses refining their operational standards to be in line with those of their leading competitors and/or accepted industry norms.

When it comes to establishing a benchmarking process there is no single methodology, but there are some guidelines that are often accepted which include:

- Selecting a specific item (or goal) to be benchmarked

- Defining or refining the process of how the item will be measured

- Identifying the sources of the data

- Collecting and analyzing the data

- Comparing the data against known standards (whether internally or industry wide)

- Drawing conclusions and making adjustments as necessary

In terms of collections, a major benchmarking goal to be measured is collecting as much as possible, as quickly as possible. Although this goal reads very simply, it’s an extensive assembly line process in which there are many parameters that must be carefully considered.

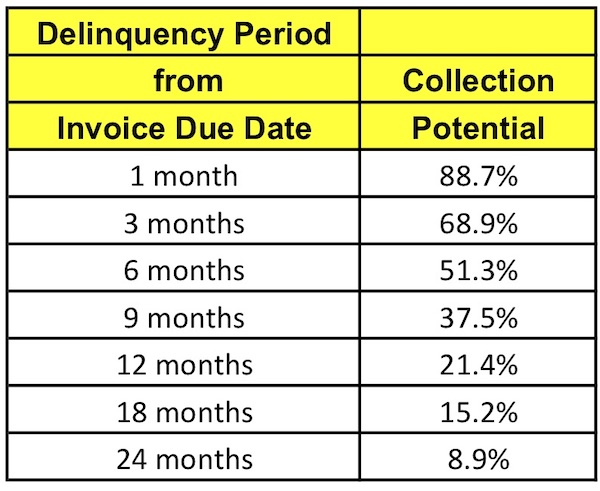

Periodically, the Commercial Collection Agencies of America (CCAA) publishes data on the potential collectability of a commercial account as follows:

In a perfect world and in view of the above data, if every time a claim at a 6-month delinquency point were placed with an outside agency, one could presume there is a 51.3% chance of collecting it in full. If it were collected, we could assume that the agency’s performance is in line with the established benchmarking data above. If it weren’t collected, a review would be required to focus on where collection efforts need improvement. In either case, without a firm understanding of the underlying parameters that impacted the result, any comparison against a benchmarking standard would not tell the whole story.

And since we work in a very imperfect commercial collection world, we need to identify the multitude of parameters involved in determining the collection potential of a claim. These parameters fall into a process I refer to as “Collectability Scoring.”

Collectability Scoring is the process of determining the collection potential of an account from the time it is placed, through the collection process, until the file is finally closed. The process includes:

- Identifying as many of a claim’s collectability parameters as possible

- Assigning a parameter rate to each parameter that will influence the collectability

- Creating a formula that logically represents how the parameter rates are utilized

- Calculating a collectability score

- Applying that collectability score to future claims which have the same or very similar set of parameters

Subsequently, the total average collectability score that results from a significant pool of all the claims with the same parameters will become the internal benchmark figure.

Let me give you a simple example using two claims.

Claim 1: Amount – $5,000, Delinquency Period – 12 months, Collector Experience – High

Claim 2: Amount – $10,000, Delinquency Period – 6 months, Collector Experience – Mid-level

Let’s start with assigning parameter rates to the claim amount. Based on an agency’s past experience, an approximate parameter rate of 70% might be assigned to all claims with amounts in the range of $5,000. In comparison, a parameter rate of 60% might be assigned to all claims with amounts of approximately $10,000.

Next, let’s factor in the parameter, delinquency period, from the CCAA data for the two claim amounts and compute a simple collectability score. On the $5,000 claim at the 12-month delinquency point, by multiplying the two parameter rates, we obtain a collectability score of (.7 x .214 = .15) 15.0%. On the $10,000 claim at the 6-month delinquency point, we again multiply the two parameter rates, which yields a collectability score of (.6 x .513 = .308) 30.8%.

Up to this point, in looking at the two claims, we can see that the delinquency period parameter plays a more significant role in the collectability score than the claim amount parameter.

Let’s now factor in the parameter for the skill of the collector, since this will also greatly impact its collectability.

- 10% for an experienced collector

- 5% for a mid-level collector

- 1% for a new collector

On the $5,000 claim at the 12-month delinquency point, being handled by an experienced collector, the formula changes slightly and for three parameter rates the collectability score would be (.7 x .214 + .1 = .25) 25.0%. On the $10,000 claim at the 6-month delinquency point, being handled by a mid-level collector, the collectability score would be (.6 x .513 + .05 = .358) 35.8%.

When you look at the collectability scores for the two claims, they are noticeably different and that’s not a bad thing because we went from only evaluating the collectability based on one parameter, delinquency, to three parameters, claim amount, delinquency, and collector experience.

You may be asking, why did we add the parameter rate for collector experience rather than multiply it against the other two parameter rates? The answer is that as we identify each parameter, we have to think about how it logically interacts into the collectability potential. It may be necessary to add, subtract, multiply, divide or perform a more complex mathematical function. In addition, you have to analyze whether the parameter should increase or decrease the collectability score.

There is no rule as to how the formula is created and developed other than to ask yourself, does it make sense and can the formula’s logic be applied to future claims? If the formula reasonably stands the test of time then it’s reliable. If not, then changes to the parameter rates and/or the formula need to be made.

Although the above examples only focused on three parameter rates, the more parameters you are able to identify as having a significant impact on the collectability score, the more refined and consistent your score will be. Simply stated, the quality of the output depends on the quality of the input.

Many parameters fall into one of the following areas:

- Claim Information Quality

- Debtor Financial Condition

- Collection System Operational Efficiency

- Creditor Response Level

- Payment Arrangement & Maintenance

Just like the benchmarking refinements mentioned at the beginning for a firearm to shoot accurately, years are often spent continuously analyzing collection data by comparing forecasted with actual results. In addition, the algorithms created are reworked many times over in order to obtain a range of accuracy that can be applied to future claims.

So where does all this take us? Although using external benchmarking figures is a good first step to understanding how well your organization is performing, it’s pulling apart and carefully analyzing the small details in the process that will truly indicate what’s happening. In doing so, you will discover the areas that need improvement and over the long term, your own benchmarking standards of operational efficiency may eventually become recognized as an integral part of the industry’s published standards.

All Rights Reserved

This article has been edited by Steven Gan.